Cost-Plus vs. Fixed-Price Construction Contracts: What Oklahoma Homebuilders Need to Know

Building your dream home is an exciting milestone, especially in Oklahoma’s thriving real estate market. Whether you are eyeing a spacious plot in Edmond, a rural acreage in Guthrie, or a custom lot in Oklahoma City, the path to homeownership involves critical decisions long before the first shovel hits the dirt.

One of the most defining decisions you will make is choosing the type of construction contract you sign with your builder. The contract structure directly impacts your budget, your financing options, and your peace of mind.

Among the various options, cost-plus contracts and fixed-price contracts are the two primary avenues. But what exactly is a cost-plus contract, and why might it not be in your best financial interest?

In this comprehensive guide, we will break down the mechanics of construction contracts, examine the hidden risks of cost-plus agreements, and show you how your contract choice interacts with your Oklahoma construction loan.

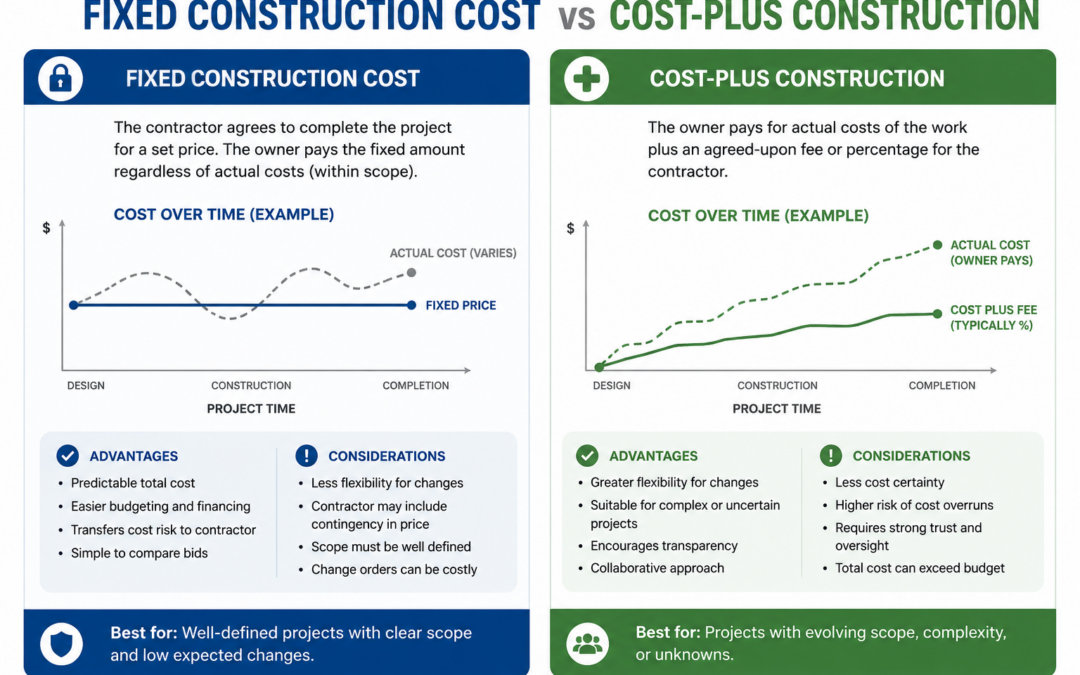

What Is a Cost-Plus Contract?

In a cost-plus contract, you agree to pay the builder for the actual cost of constructing your house plus a predetermined fee. This fee is typically structured as a percentage of the overall building costs (e.g., actual expenses plus 10% to 15% profit) or, less commonly, a flat fixed fee on top of fluctuating expenses.

At first glance, this type of contract can be highly enticing. It gives home buyers the impression that they are gaining total freedom, flexibility, and authority over the building process. If you decide mid-construction that you want to upgrade your kitchen countertops or expand the master closet, a cost-plus contract accommodates those changes seamlessly because you simply pay the difference plus the builder’s percentage fee.

Because the price isn’t set in stone, a cost-plus builder is also much more likely to say “yes” to complex, highly customized home designs. They face no personal financial risk if the project becomes more complicated or more expensive than originally anticipated. Even if the builder knows deep down that your ambitious design will go significantly over your initial target budget, they have little reason to object because their compensation is tied directly to the final tally.

Why Isn’t a Cost-Plus Contract in Your Best Interest?

While the flexibility of a cost-plus contract sounds wonderful on paper, the reality can be a financial nightmare for the average homeowner.

1. The Total Lack of Accountability

Simply put, without a fixed price, there is absolutely nothing to hold the builder accountable to your budget.

Let’s look at a realistic scenario: You tell your custom home builder that your absolute maximum budget for the physical build is $250,000. Under a cost-plus framework, that number is merely an estimate—it is not a binding constraint. The builder does not have a legal obligation to stay within that price range. If lumber prices suddenly spike, or if the excavation team encounters unexpected rocks on your Oklahoma lot, those added expenses are passed completely on to you.

2. A Built-In Incentive to Spend More

Perhaps the most dangerous aspect of a percentage-based cost-plus contract is the backward incentive structure. There is zero financial incentive for a cost-plus builder to stay within budget or actively reduce waste during construction.

In fact, there is a built-in incentive for the builder to let the project go over budget. Consider the math:

-

If your home costs $250,000 to build and the builder’s fee is 10%, they make $25,000.

-

If inefficiencies, delays, or premium material swaps push the final build cost up to $350,000, that same 10% fee nets the builder $35,000.

Ultimately, the more money you spend and the more the project goes over budget, the more profit the builder takes home. This structural flaw leaves you incredibly vulnerable to blowing up your budget and jeopardizing your entire construction project.

Fixed-Price Construction Contracts: The Stable Alternative

If a cost-plus contract shifts all the financial risk onto your shoulders, a fixed-price construction contract does the exact opposite. It holds your builder strictly accountable.

In a fixed-price contract, the agreed-upon budget is the gospel truth. When you select a custom home plan and present it to your builder, they must thoroughly calculate the material costs, labor, and contingencies upfront. They will then compile a binding contract that guarantees the delivery of that exact home for a specific dollar amount, integrating the design features you love without exceeding your stated budget limit.

Who Pays for Inefficiency?

The core difference between these two contracts comes down to a simple question: Who do you want to pay for construction inefficiency—you or your builder?

| Feature / Scenario | Cost-Plus Contract | Fixed-Price Contract |

| Price Predictability |

Unpredictable; changes with material and labor shifts. |

Guaranteed upfront price. |

| Risk of Material Cost Spikes | Borne entirely by the homeowner. |

Borne entirely by the builder. |

| Builder Incentive |

Incentivized to let costs rise to increase percentage fee. |

Incentivized to work efficiently to preserve profit margin. |

| Financial Accountability |

No built-in mechanism to cap spending. |

Strict budget boundaries enforced by contract law. |

Under a fixed-price contract, the builder who constructs your home on your lot must operate with high efficiency. If they make a mistake, order the wrong supplies, or manage their subcontractors poorly, they cannot pass those costs along to you. The builder eats the extra cost.

No one wants to be caught off guard by a surprise $30,000 bill three weeks before moving in. This is why securing a fixed-price construction contract is highly recommended to protect your finances, regardless of which builder you choose.

How Construction Contracts Impact Your Mortgage Financing

Choosing a contract isn’t just a matter of personal preference; it also directly influences your ability to secure home financing. Lenders look closely at contract structures to assess risk before approving a loan.

The Danger of Cost Overruns with Construction Loans

When you apply for a residential construction loan, the lender evaluates the project based on the initial builder estimates, architectural plans, and a professional appraisal. If you use a cost-plus contract and the project experiences severe cost overruns, you run into a massive roadblock: the lender will not automatically increase your approved loan amount.

If construction costs exceed the original estimates under a cost-plus agreement, you are solely responsible for covering those cost overruns out of pocket. For instance, Spurr Mortgage generally advises clients to budget a 5% contingency reserve for unexpected costs like sudden material price changes or site preparation challenges. However, a cost-plus contract can easily blow past a 5% safety net, leaving you forced to find tens of thousands of dollars in cash mid-build or face an unfinished home.

Appraisals and Loan-to-Value Realities

Before construction begins, your lender orders a “subject to completion” appraisal. This estimate evaluates what the home will be worth after it is fully built, comparing it to recent home sales in areas like Edmond or surrounding Oklahoma counties.

If your cost-plus builder allows inefficiencies to drive the physical build cost to $400,000, but the local Oklahoma market appraisal determines the finished home is only worth $340,000, your loan-to-value (LTV) ratio is disrupted. The lender will cap your financing relative to the appraised market value, leaving you to bridge the entire valuation gap with your own funds. A fixed-price contract protects you from this dynamic by tying the actual cost directly to the market-supported specifications from day one.

Financing Your Build the Right Way in Oklahoma

Whether you find a builder offering a secure fixed-price arrangement or you require strategic advice on managing builder contracts, navigating custom home financing requires local expertise. At Spurr Mortgage, we specialize in simplifying the path to building your custom home across Oklahoma.

The Power of the One-Time Close Construction Loan

To maximize your savings and minimize your stress, we recommend exploring a One-Time Close (OTC) Construction Loan (also known as a Construction-to-Permanent loan). This innovative program combines short-term construction financing and your long-term permanent mortgage into a single transaction.

The advantages of a One-Time Close Loan include:

-

Single Closing Process: You pay closing costs only once, saving thousands of dollars compared to traditional two-closing loans.

-

Rate Protection: Secure your interest rate upfront with a complimentary float-down option, allowing you to capture lower market rates if they drop during the 6 to 12 months your home is being built.

-

Automatic Conversion: Once your final inspection is complete, your loan seamlessly transitions into a standard 15- or 30-year fixed mortgage with no re-qualification or second application required.

-

Interest-Only Payments: During the active construction period, you only make monthly interest payments on the funds that have been drawn to pay for completed construction milestones.

Flexible Options for Every Homebuyer

We offer various avenues tailored to your specific financial situation:

-

Conventional OTC Financing: Up to 95% Loan-to-Value (LTV) with as little as a 5% down payment, supporting loan amounts up to $832,750.

-

FHA Construction Loans: Ideal for first-time buyers looking to preserve cash, offering down payments as low as 3.5% (up to 97.5% LTV) for loan amounts up to $541,287.

-

VA and USDA Options: Eligible military veterans can access 100% financing with zero down payment, while rural homebuyers can look into specialized USDA construction financing based on regional income guidelines.

Build with Confidence with Spurr Mortgage

Don’t let confusing builder contracts or complex financing processes stall your dream of building a home in Oklahoma. By choosing a transparent, accountable contract structure and partnering with an experienced local lender, you can step onto your new homesite with complete peace of mind.

If you are ready to establish your budget, look for land, or vet your builder’s qualifications, our dedicated team is here to guide you through every step—from pre-approval to your final walk-through.

Ready to take the first step toward your new home? Contact Jennifer Buffington, Senior VP and Construction Loan Specialist at Spurr Mortgage.

Phone: 405-348-9919 (Office) or 405-201-4829 (Cell)

Email: Jennifer@spurrmortgage.com

Office Address: 233 E. 10th Street Plz, Edmond, OK 73034

All loans are subject to credit approval, property eligibility, income limitations, and program guidelines